As the EU pushes on to achieve climate neutrality by 2050, emissions tracking, reporting, and reduction are among the main focal points of both national and joint regulatory bodies in Europe. With that said, the complex nature of modern businesses necessitates a layered, systematic approach. Regarding greenhouse gas (GHG) emissions in particular – an umbrella term for CO2, methane (CH₄), nitrous oxide (N₂O), fluorinated gases, and other gasses that trap heat in the atmosphere – the main distinction is reflected in 3 scopes. Scope 1 reflects direct emissions from a company‘s owned or controlled activities, Scope 2 emissions are indirectly generated from purchased energy consumed by a company, and Scope 3 defines emissions that occur in a company‘s value chain but are not directly owned or controlled by the company.

Scope 3 addresses the value chain in both directions: upstream and downstream. Tracking and reporting scope 3 emissions is a complex task, but the prospect of establishing unified guidelines shows a lot of potential in relation to decarbonization targets in the EU. A strong indicator here is the fact that Scope 3 emissions can account for around 90% of a company‘s total carbon footprint, although precise numbers vary by industry [1]. Since value chains often include multiple stages of a product or service‘s lifecycle, including material sourcing, distribution, and end-of-life treatment [2], the involvement of all stakeholders is a prerequisite for making a real impact. In parallel, regulatory initiatives target this complex cascading system of emissions distributed throughout the layers of the economy at a broad angle. The result of this approach is a highly intricate, multi-layered system of regulatory requirements. Filtering these measures according to industry and other relevant business variables is meant to allow businesses to gain a detailed picture of the required changes and implement them in a targeted, effective way.

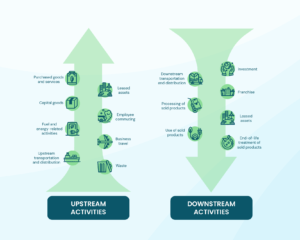

Scope 3 emissions in logistics: overview of focal points and value chain complexity

In official accounts, Scope 3 emissions fall into 15 categories that are further divided into two main types: Upstream and Downstream [3].

Their relevance to companies in the logistics sector largely varies case by case, but two categories in particular have a specific focus on this industry: upstream transportation and distribution, and downstream transportation and distribution.

Category 4 – upstream transportation and distribution – includes GHG emissions produced during the transportation and distribution of raw materials, components, and finished goods before they arrive at the reporting company. It accounts for emissions from vehicles and vessels (e.g., trucks, trains, ships, aeroplanes) used to transport goods, as well as emissions from warehousing and storage facilities prior to the goods being received by the company [4]. Tracking and reporting Scope 3 emissions of this origin offers supply chain insights that are crucial to optimizing logistics operations, in turn enabling businesses to address stakeholder and customer expectations related to transparency and sustainability [5].

Category 9 – downstream transportation and distribution – includes GHG emissions produced during the transportation and distribution of products sold by a company after they leave its control. It accounts for emissions related to warehousing, retail, chosen transport modes, and distance traveled [6]. Addressing these emissions requires a collaborative approach across the supply chain: alongside tracking and reporting Scope 3 emissions, businesses can also engage in co-creation, working together with logistics partners to optimize supply chains, enhance route efficiency, explore targeted fleet electrification, and develop more effective sustainability strategies. This shared effort helps companies meet evolving stakeholder and customer expectations while contributing to broader industry-wide sustainability goals [source].

In terms of the tracking itself, both upstream and downstream emissions related to transportation and distribution can be calculated based on distance traveled, weight of goods, or mode of transport [7]. A significant point to consider here is that certain types of transportation (rail, for example) produce significantly fewer emissions than others (air transport, for instance). Additionally, alternative fuels like HVO (Hydrotreated Vegetable Oil) offer a viable way to reduce carbon emissions without requiring major fleet modifications. Partnering with logistics providers like Girteka, which actively invests in sustainable solutions, is a solid opportunity to reduce Scope 3 emissions while improving overall supply chain efficiency.

Coming back to the general notion of GHG emissions tracking, a significant figure related specifically to the logistics sector attributes 40-50% of total emissions to Scope 3. Given that the logistics sector accounts for approximately 8% of global CO₂ emissions [8], this figure not only justifies the regulatory focus but also highlights the tangible potential of effectively implemented emissions tracking measures. Moreover, understanding and tracking GHG emissions related to transportation and distribution promises not only improved operational efficiency but also a more resilient and sustainable business trajectory.

Challenges in Scope 3 emissions reporting

While the share of emissions generated by the logistics sector highlights the tangible benefits of effective emissions tracking, the complexity of establishing consistent, systematic GHG tracking and reporting still gets downplayed. With regulatory bodies targeting climate neutrality by 2050, the demand for – and the variety of – emerging methodologies, guidelines, and digital tools to choose from is high. However, the real challenge lies in determining which approaches deliver the most benefits, and in developing a robust, consistent tracking and reporting system that will yield lasting results.

Some of the main challenges businesses face on their path in relation to Scope 3 emissions reporting include issues with data availability and quality, value chain complexity, and the absence of standardization in reporting practices. For companies whose value chains include hundreds or even thousands of partners, emissions data collection can be a challenging endeavor. Additionally, not all companies have the in-house knowledge and personnel needed for providing the required data in the first place [9]. The more partners there are, the wider the list of issues may be when – or rather if – there is a willingness to share emissions reports at all. The latter issue is mostly tied to small companies, which may fail to understand the importance of emissions estimation in light of the initial investments needed to put the necessary systems or practices in place.

The issue of limited data availability and quality further highlights the ongoing lack of standardization. Since Scope 3 emissions are generated by third parties, the reporting company has limited visibility and/or control over how data is collected and transferred [10]. Aggregating data and estimating emissions from hundreds or even thousands of partners that do not use a unified emissions calculation method adds a new level of complexity to an already challenging task, requiring significantly more resources and time—an outcome that is counterintuitive given the initial purpose of GHG emissions reporting. A proactive approach to this challenge includes partnering with a single logistics provider that offers standardized reporting and modern data solutions.

Best practices for transparent Scope 3 emissions reporting

Although the outline of the main challenges in Scope 3 emissions reporting reflects a spectrum of issues, ineffective communication with suppliers can be seen as an underlying reason – and a powerful solution in disguise. Since achieving Scope 3 targets is a shared effort between businesses and their suppliers, progress depends on mutual engagement and collaboration. Co-creating decarbonization strategies where companies work alongside their logistics partners to align sustainability goals, investment priorities, and operational decisions is essential for ensuring steady progress on the sustainability front, and long-term partnership success as well.

The case of Danone, a leading global food and beverage company, serves as a solid example to the possible impact of improved communication with suppliers – 120,000 of them, to be exact. In 2015, Danone committed to reduce its Scope 1, 2, and 3 emissions by 50% between 2015 and 2030. Since many of their suppliers are subsistence farms with fewer than ten cows, Danone developed a framework of representative farms across the globe that are monitored daily, and extrapolates data from these farms to similar ones. To measure the emissions impact of the farms, Danone also adopted a digital tool, Cool Farm [11].

Indeed, another effective solution for companies looking to optimize their Scope 3 emissions tracking and its impact is the adoption of software tools. This is an important step in the wider process of automating data collection, which is meant to reduce manual effort and errors [12]. To further improve emissions reporting, businesses can use their digital platforms to integrate real-time tracking, advanced data visualization via dashboards, and centralized communication. As a result, when it comes to choosing a future-ready logistics provider, for instance, partnering with a well-digitalized company opens doors to clearly structured and verifiable data, making reporting more transparent and aligned with best practices in the industry.

Frameworks and regulations for Scope 3 emissions reporting

Despite the lack of standardization in reporting practices, proven methodologies offer a structured approach to data collection and emissions reduction. Among the most widely recognized methodologies today are the GHG Protocol’s Corporate Value Chain (Scope 3) Standard and the Smart Freight Centre’s GLEC Framework.

The GHG Protocol requires companies to report all GHG emissions in metric tons of CO₂e and include Scope 3 emissions intensity metrics for all relevant activities. Companies must disclose their chosen base year (with rationale) and any reductions in absolute emissions and intensity since that year. Reporting should follow five guiding principles: relevance, completeness (with justification for any exclusions), consistency, transparency, and accuracy [13].

The GLEC Framework stands out due to its full alignment with the updated ISO 14083 standard. Offering a systematic approach to calculating the carbon footprint of the global logistics supply chain, it provides guidance on setting boundaries and sourcing data across the entire transport chain, with reporting requirements that range from basic “must-have” metrics to advanced levels for high improvement potential [14].

As companies strive for greater accuracy in emissions reporting, regulatory pressure is also increasing. On the regulatory front, significant changes are in motion under the EU Corporate Sustainability Reporting Directive (CSRD). Building on the NFRD, it introduced more detailed requirements, significantly expanding the number of companies required to report—nearly 50,000 compared to 11,000 under the NFRD. It applies to large EU companies meeting at least two of the following criteria—€40 million in net turnover, €20 million in assets, or 250+ employees—and to non-EU companies with €150 million in EU turnover. Implementation is phased, with large public-interest entities reporting by 2025, other large companies by 2026, and listed SMEs by 2027 (with an opt-out until 2028) [15].

Takeaways and future prospects

As examples and studies discussed above show, Scope 3 emissions tracking and reporting offers lasting benefits that extend well beyond the immediate industry of companies in question, supporting broader sustainability goals and contributing to a climate-neutral future. Specifically with regard to logistics providers, choosing a partner that prioritizes data transparency and invests in future-ready solutions simplifies Scope 3 emissions calculations, mitigates risks, and unlocks new opportunities for innovation and collaboration.

Adopting proven methodologies and maintaining transparent reporting practices across the entire value chain also offers a future-proof approach to upcoming regulatory requirements. Early adoption in particular reinforces a company’s reputation, positioning it as a forward-thinking, responsible organization. Speaking of the very first steps in this direction, strong communication and aligned sustainability goals with all stakeholders can be seen as a turning point – both for immediate and long-term success. By engaging leadership, adopting a common language, and leveraging digital tools, companies can foster collaboration that drives continuous improvements in emissions management from within.